http://euromaidanpress.com/2016/04/18/91786/

At his annual phone-in event with the Russian people on April 14, President Putin struck an optimistic note and projected that Russian GDP would contract by only -0.3% in 2016 and would grow 1.4% in 2017. Only days earlier, the IMF released its

World Economic Outlook report and projected a fall in Russian GDP in 2016 of -1.8%, growth of 0.8% in 2017, and growth of 1.5% through 2021.

Russia’s economic growth is

really two problems. It has to return to

growth and it has to keep up with other countries in order not to fall behind

economically. If Russia does not grow

and if it does not grow as fast as other countries, Russia will, in a curious

reversal, grow less developed because investment will be insufficient to renew

its aging economic infrastructure. Oil

and gas, for instance, will require

massive investment to maintain production and to exploit more difficult fields.

Russia must attract new investment that

is used productively. That said, let’s

see how Russia is doing based on comparisons using the IMF’s latest data.

One comparison is how Russia is doing in relation to the Commonwealth of Independent States (CIS),

the collection of countries that were once part of the Soviet Union. According to the IMF, the “CIS-minus-Russia”

is expected to grow by 0.9% in 2016, 2.3% in 2017 and 4.2% by 2021. In its own backyard, Russia is expected to be

a laggard. In fact, from 2017 when Russia

hopes to return to growth through 2021 the IMF expects Russia to be the worst

performer among CIS countries, with the exception of Belarus (which seems

unfair since Belarus doesn’t have oil or gas, didn’t support Russia’s

annexation of Crimea or invasion of eastern Ukraine, and has nothing to do with

Syria—but economics is unforgiving).

One comparison is how Russia is doing in relation to the Commonwealth of Independent States (CIS),

the collection of countries that were once part of the Soviet Union. According to the IMF, the “CIS-minus-Russia”

is expected to grow by 0.9% in 2016, 2.3% in 2017 and 4.2% by 2021. In its own backyard, Russia is expected to be

a laggard. In fact, from 2017 when Russia

hopes to return to growth through 2021 the IMF expects Russia to be the worst

performer among CIS countries, with the exception of Belarus (which seems

unfair since Belarus doesn’t have oil or gas, didn’t support Russia’s

annexation of Crimea or invasion of eastern Ukraine, and has nothing to do with

Syria—but economics is unforgiving).

Another comparison might be the IMF’s Emerging and Developing Europe (EDEU) group, including such

struggling countries as Kosovo and Serbia, but also Hungary and Poland. Here, Russia fairs worse. EDE is expected to grow by 3.5% in 2016 and

by 3.3% thereafter through 2021, more than twice as fast as Russia.

Still another comparison might be with the European Union, that body of Western

democracies that Putin believes is on the verge of economic collapse and whose collapse

he earnestly promotes. There is little

comfort in the projections though. The

IMF expects the EU to grow about 1.8% from 2016 through 2021. Even by 2021, the IMF does not expect Russia

to catch up with Putin’s enfeebled European Union. Although Russia and the EU’s growth rates

converge, with the EU growing slightly faster, it is not the company Putin

hoped to keep.

Still another comparison might be with the European Union, that body of Western

democracies that Putin believes is on the verge of economic collapse and whose collapse

he earnestly promotes. There is little

comfort in the projections though. The

IMF expects the EU to grow about 1.8% from 2016 through 2021. Even by 2021, the IMF does not expect Russia

to catch up with Putin’s enfeebled European Union. Although Russia and the EU’s growth rates

converge, with the EU growing slightly faster, it is not the company Putin

hoped to keep.

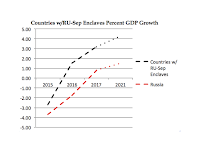

How about comparison with the states where Russia maintains Russian-separatist enclaves, Georgia,

Ukraine and Moldova? Again, things don’t

look so good. The three states are

expected to average growth of 1.5% in 2016, 3.2% in 2017 and 4.3% by 2021,

nearly three times as fast as Russia. So

much for economic subjugation through conquest.

How about comparison with the states where Russia maintains Russian-separatist enclaves, Georgia,

Ukraine and Moldova? Again, things don’t

look so good. The three states are

expected to average growth of 1.5% in 2016, 3.2% in 2017 and 4.3% by 2021,

nearly three times as fast as Russia. So

much for economic subjugation through conquest.

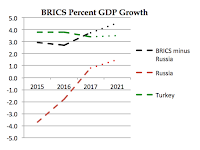

Perhaps further afield, among the BRICS? As a group, the “BRICS-minus-Russia” (Turkey

added separately for interest) are projected to grow at 2.7% in 2016, 3.7% in

2017 and 4.3% by 2021. Even beleaguered

South Africa manages to outpace Russia by a large margin. Only Brazil does worse, declining -3.8% this

year and next, although by 2021 Brazil is projected to also overtake Russia by

a wide margin. Brazil, as a fellow

underperformer, should give Putin pause.

Racked by corruption and economic mismanagement, as of this writing Brazil

is set to impeach its President, herself like Putin an old communist

apparatchik. In fact, as described by

the Financial

Times, plans to reform Brazil’s economy sound a lot like what Russia

needs. The Times quotes Brazil’s

Vice President Temer as saying, “What’s

needed is tighter fiscal policy, lower interest rates, a weak currency, and

eventually structural reforms to raise savings and investment.” The other underperformer, South Africa,

although it outperforms Russia, suffered the same political crisis as Brazil, with

its President Zuma narrowly escaping impeachment. Economically speaking--as a BRIC in economic

crisis--Russia sits in the uncomfortable company of South Africa and Brazil, an

association Putin should find politically uncomfortable.

Perhaps further afield, among the BRICS? As a group, the “BRICS-minus-Russia” (Turkey

added separately for interest) are projected to grow at 2.7% in 2016, 3.7% in

2017 and 4.3% by 2021. Even beleaguered

South Africa manages to outpace Russia by a large margin. Only Brazil does worse, declining -3.8% this

year and next, although by 2021 Brazil is projected to also overtake Russia by

a wide margin. Brazil, as a fellow

underperformer, should give Putin pause.

Racked by corruption and economic mismanagement, as of this writing Brazil

is set to impeach its President, herself like Putin an old communist

apparatchik. In fact, as described by

the Financial

Times, plans to reform Brazil’s economy sound a lot like what Russia

needs. The Times quotes Brazil’s

Vice President Temer as saying, “What’s

needed is tighter fiscal policy, lower interest rates, a weak currency, and

eventually structural reforms to raise savings and investment.” The other underperformer, South Africa,

although it outperforms Russia, suffered the same political crisis as Brazil, with

its President Zuma narrowly escaping impeachment. Economically speaking--as a BRIC in economic

crisis--Russia sits in the uncomfortable company of South Africa and Brazil, an

association Putin should find politically uncomfortable.

As bad as it looks, it is

probably worse. Not only does Russia

perform poorly against comparator groups, it is likely to do worse than the IMF

projects. The problem is not oil or

sanctions, although these make the situation more difficult. The problem is that growth in Russia was

falling for years before the fall in oil prices in 2014 and the imposition of

sanctions. Already in 2013, Russian

growth had fallen to 1.3% because of lack of investment. In 2014 and 2015 investment fell

steeply. This suggests that Russia will

struggle to achieve growth of even 1.3%--if it is even possible--for the

foreseeable future because there is nothing to drive a reversal in declining

investment. Without undertaking reform measures

recommended by the IMF or, for that matter, by Alexei Kudrin, Russia will fall

short of the IMF’s 2017-2021 projection and be that much more behind its

comparators.

Put it all together and the

chart to the left is how the IMF expects Russia to compare in 2021. For a country that aspires to be a great

nation and to lead an alternative international world order to the democratic

West, this is not the path to power or to greatness. It is the path of growth in reverse

to lesser and lesser significance, if Russia does not correct course. Like the character in the film The Curious Case of Benjamin Button,

Russia may find itself regressing to a less developed state while

the rest of the world grows.

Dirk

Mattheisen is a writer and blogger on political

economy with a focus on European affairs. He is also an independent

consultant on institutional governance of international economic and financial

institutions. Dirk Mattheisen is a former Assistant Corporate

Secretary of The World Bank Group.

Dirk

Mattheisen is a writer and blogger on political

economy with a focus on European affairs. He is also an independent

consultant on institutional governance of international economic and financial

institutions. Dirk Mattheisen is a former Assistant Corporate

Secretary of The World Bank Group.